|

|

为让大家更方便的阅读老方的文章,老方把自己的文章做了一下汇总,分为

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之房产篇

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之教育篇

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之医疗篇

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之交通篇

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之生活常识篇

卡尔加里老方:【收藏】加拿大卡尔加里全攻略之吃喝玩乐篇

等系列送给大家,如有新文章会及时更新,收藏即可:)

卡尔加里11月1日讯:

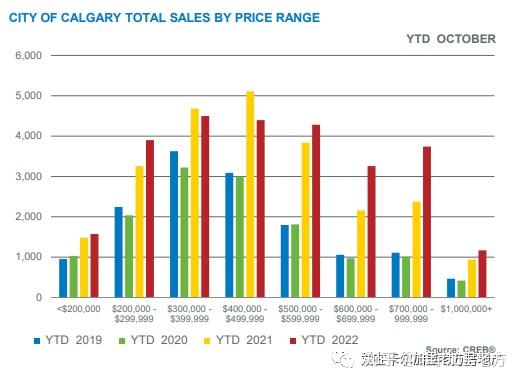

卡城10月房产销量同比有所下降,主要是独立屋板块的销售放缓造成的。

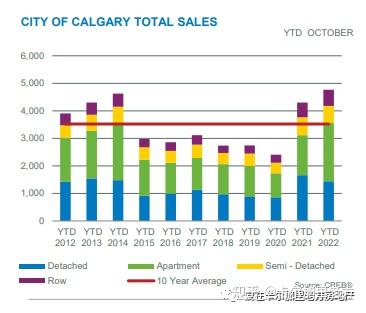

不过,10月1857套的销量仍远高于长期平均和疫情前水平。年初至今的房屋总销量达到了26823套,离年底还有两个月,2022年卡城房产的总销量将是破纪录的。

“由于对低总价高密度住宅产品的持续强劲需求,卡尔加里房地产销量并没有像加拿大其它大城市那样大幅回落。但卡城并不是对通过膨胀和高利率免疫,而是强劲的就业增长,人口净流入和旺盛的大宗商品(石油)市场,抵消了一些负面影响。” 卡尔加里地产经纪协会首席经济师 Ann-Marie Lurie这样总结到。

【专注于加拿大西部房地产投资的财经媒体Western Investor,本周发布了最新的投资报告,其中列出了加拿大西部2023年最适合房地产投资的五个地区。卡尔加里以充足的工作机会和房地产的可负担性,位居榜首;剩下的4个都在BC省。

图源:ShutterStock

第一名

卡尔加里

作为阿尔伯塔省最大的城市,卡尔加里仅在9月就承诺提供2600个新的高薪工作岗位;房地产价格比温哥华低很多;没有租金管制;油价全国最低。种种这些有利条件都说明,投资卡尔加里房地产市场的时机已经成熟。

图源:ShutterStock

9月下旬,加拿大德哈维兰飞机公司(De Havilland Aircraft of Canada)宣布,它在卡尔加里以东的惠特兰县购买了3700英亩的土地,并计划兴建一个工厂,进行飞机制造和维修,预计建成后将雇用1500名员工。

几天后,9月26日,印度全球科技巨头Infosys官宣其在卡尔加里市中心的数字中心开幕,约20万平方英尺的办公室将创造1000个工作岗位。Infosys是下一代数字系统的领导者,自2021年公司首次扩展到加拿大以来,其最初的招聘承诺已经翻倍。

Infosys的总裁在发布会上表示,“今天将开启我们在加拿大的新篇章。卡尔加里的信息技术创新潜力是无限的,我们很高兴成为其未来的一部分。”

石油和阿尔伯塔省的经济息息相关。今年春天,油价曾经飙涨到每桶130美元,尽管在10月份回落到每桶89美元,仍然是2014年油价低点时的两倍,并且明年还将继续驱动阿尔伯塔省的经济发展。

图源:ShutterStock

根据加拿大智库Conference Board of Canada的数据,卡尔加里的实际GDP增长,预计在2022年可以达到6.3%,2023年达到3.8%,远超加拿大1.2%的平均增长预期。

卡尔加里的商业房地产市场是工业部门主导的,空置率极低,仅为2.2%,平均租金为每平方英尺11.65加元,大约是温哥华的一半。这让卡尔加里吸引了不少来自BC省的企业。

图源:ShutterStock

受每个月稳定的80亿元消费支出吸引,投资者也正在涌入卡尔加里的零售行业。多单位住宅市场同样火爆,因为其价格与温哥华和多伦多相比实在是便宜太多了。

凭借着强劲的就业机会、较低的省税、高比例的移民以及友好的商业环境,从现在到2023年,卡尔加里都是当之无愧的投资首选。】

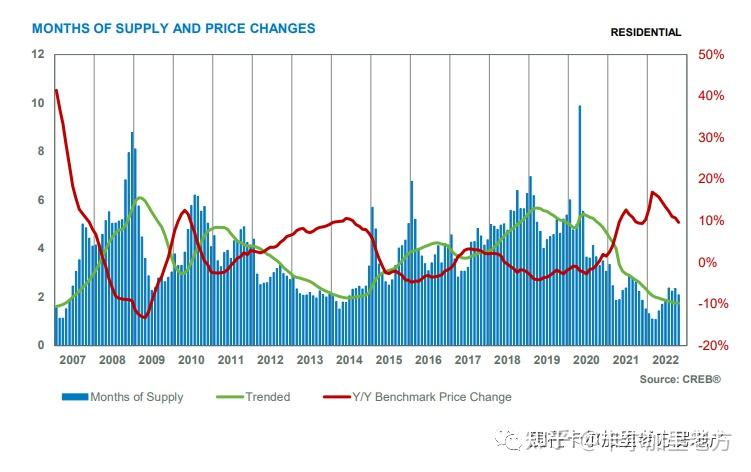

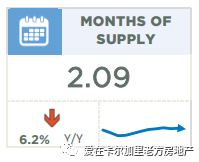

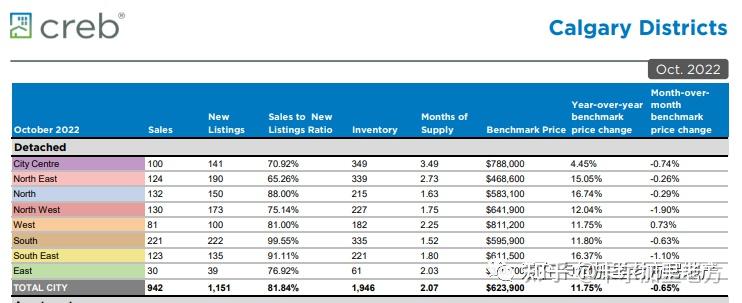

新上市量也下降了,导致这个月的挂牌成交率达到了85%,库存也有所下降。库存量的减少主要是50万以下的房产贡献的。

虽然房地产市场不像今年上半年那么紧张了,但只有2个月房屋供应月数,比历史平均要紧张多了。

当然,不同的板块表现不尽相同,低总价板块仍是卖方市场,高端板块则趋向平衡。

10月,卡城房价比今年5月的高点回落了4%。和加拿大的其它大城市相比,这算是相对很小的调整了。需要着重指出的是,卡城10月房产的基准价格同比仍高近10% 。

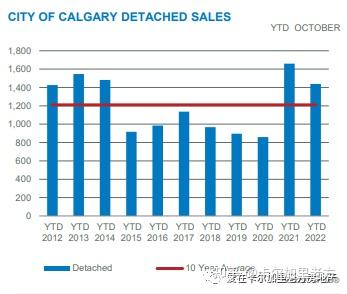

独立屋

Detached

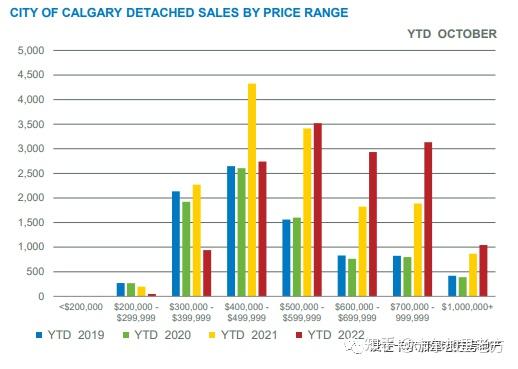

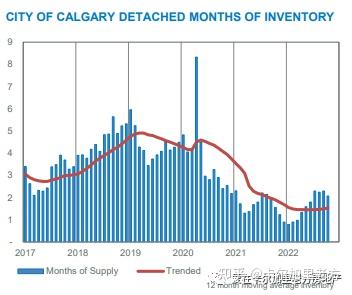

10月70万以上的独立屋销量同比增加,但不足以抵消低总价独立屋销量的下降,10月独立屋销量同比大降29%。低总价独立屋供应持续严重短缺,让该板块市场条件异常紧张。

10月,卡城独立屋库存低于2000套,比该月的历史平均水平低近35%。

在这2000套库存中,高总价占比42%。这有可能造成不同的价格区间,独立屋的价格走势会不一样。

总体而言,独立屋的价格环比暨比5月高点略降,但同比让涨12%。其中涨幅最大的是北区和东南区。

双拼

Semi-Detached

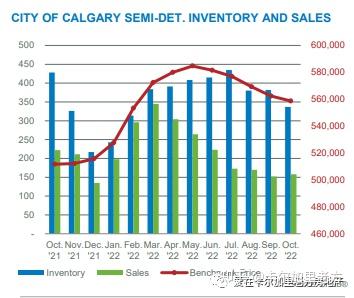

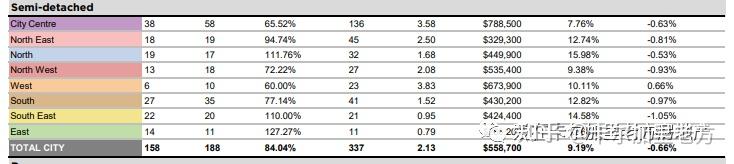

10月双拼销量同比略降,不过最近的销量下降难以撼动上半年的销量涨幅,年初至今的总销量同比涨近3%。

新上市量也下降了,把这个月的挂牌成交率推高到了80%,房屋供应月数才2个月多一点。

双拼的基准价格环比略有下降,同比仍涨9%。

年度价格涨幅从市中心区的不到8%到北区的16%不等。

联排

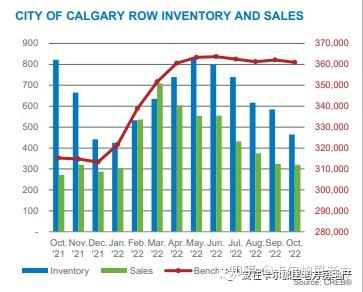

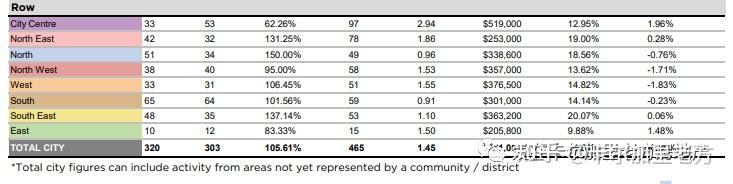

Row

10月联排销量同比继续增长,年初至今联排总销量同比涨42%。于此同时,新上市量却在下降,使得这个月的挂牌成交率达到了106%。

库存下降,销量增长,只有两个月不到的房屋供应月数,联排板块现在是妥妥的卖方市场。这也让联排的价格持续坚挺。

10月,联排的基准价格是 $361,200,只比今年6月的高点降1%。

总体而言,联排价格同比涨了近15%。其中涨幅最大的是东南区‘东北区和北区。

公寓

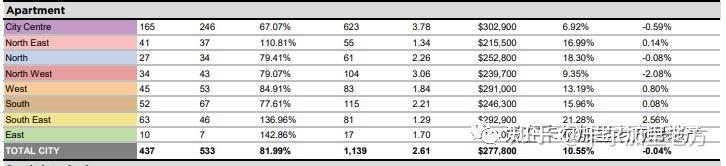

Apartment Condominium

10月公寓销量同比也继续增长,年初至今的总销量同比涨56%。新上市量也在增长,不过涨幅赶不上销量的涨幅,所以公寓库存有所下降。

10月公寓房屋供应月数只有三个月不到,是2013年以来10月最低的。

10月公寓基准价格$277,800,环比持平,同比涨11%。

涨幅最大的区域都在市中心区之外。虽然价格已连续几个月上涨,仍比2014年的高点低9%。

常用房地产统计术语:

挂牌成交率(the sales-to-new listings ratio):给定期间的当前销售套数对比新上市套数,一般采用过去30天的数据。此比率一般是一个百分数,如果在40-60%之间,代表市场比较平衡,如果高于60%,一般指卖方市场,如果低于40%,一般代表买方市场。

房屋供应月数(Months of Supply):给定时间段(通常是过去30天)结束时库存总数除以同一时期结束时的销售总数。库存月数是房屋供求平衡的另一重要指标。它代表以目前的销售活动完全清算当前库存需要多长时间。

City of Calgary, Nov. 1, 2022 – October sales eased compared to last year’s levels, mostly due to slower activity in the detached sector.

However, with 1,857 sales this month, levels are still stronger than long-term trends and activity reported prior to the pandemic. Year-to-date sales have reached 26,823 and with only two months to go, 2022 will likely post a record year in terms of sales.

“Calgary hasn’t seen the same degree of pullback in housing sales like other parts of Canada, thanks to persistently strong demand for our higher density product,” said CREB® Chief Economist Ann-Marie Lurie. “While our city is not immune to the impact that inflation and higher rates are having, strong employment growth, positive migration flows and a stronger commodity market are helping offset some of that impact.”

New listings also trended down this month causing the sales-to-new-listings ratio to rise to 85 per cent and inventories to trend down. Much of the inventory decline has been driven by product priced below $500,000.

While conditions are not a tight as what was seen earlier in the year, with only two months of supply, conditions remain tighter than historical levels. We are also seeing divergent trends in the market with conditions continuing to favour the seller in the lower-price ranges and shifting to more balanced conditions in the upper-price ranges.

As of October, prices have eased by four per cent relative to the highs reached in May. This is considered a relatively small adjustment when considering price movements in other large cities. It is also important to note that the October benchmark price is still nearly 10 per cent higher than levels reported last year.

Detached

Sales growth in the over $700,000 price range this month were not enough to offset the declines in the lower-price ranges, causing detached sales to ease by over 29 per cent compared to last year. Limited supply growth in the lower-price ranges continue to keep conditions exceptionally tight for lower-priced detached homes.

In October, inventory levels for detached homes were under 2,000 units, nearly 35 per cent lower than typical levels reported for the month. Moreover, over 42 per cent of the inventory falls in the upper-price ranges of the market. This is likely creating a situation where pricing trends will vary depending on price range.

Overall, detached prices did trend down relative to last month and peak levels in May but remain nearly 12 per cent higher than levels reported last October. The strongest year-over-year price gains have occurred in the North and South East districts.

Semi-Detached

While sales remain lower than last year’s levels in October, recent pullbacks have not offset gains from earlier in the year and year-to-date sales improved by nearly three per cent. A pullback in new listings relative to sales caused the sales-to-new-listings ratio to push above 80 per cent this month and inventories to ease, leaving the months of supply just over two months.

The benchmark price, while easing slightly compared to last month, remained over nine per cent higher than last year’s levels. Year-over-year price gains have varied from a low of nearly eight per cent in the City Centre to a high of 16 per cent in the North district.

Row

Row sales continue to rise relative to last year supporting a year-to-date gain of nearly 42 per cent. At the same time, new listings this month eased ensuring that the sales-to-new-listings ratio remain exceptionally tight at 106 per cent. Falling inventories and improving sales have ensured this market continues to favour the seller with less than two months of supply. This has also prevented the same adjustment in price.

As of October, the benchmark price was $361,200, less than one per cent lower than the peak achieved in June of this year. Overall, prices remained nearly 15 per cent higher than last year’s levels. The strongest price gains occurred in the South East, North East and North districts.

Apartment Condominium

Apartment sales continue to rise over levels reported last year contributing to the year-to-date increase of over 56 per cent. Improving sales were also met with gains in new listings, but as the growth in sales outpaced the new listings activity, inventory levels continue to trend down. As of October, the months of supply remained just below three months, the lowest level recorded in October since 2013.

In October, the benchmark price was $277,800, similar to last month and nearly 11 per cent higher than last year’s levels. Some of the strongest price gains have occurred in areas outside of the City Centre. Despite persistent price growth, overall prices remain nine per cent below previous highs set back in 2014.

REGIONAL MARKET FACTS

Airdrie

Easing sales over the past several months have not been enough to offset earlier gains as year-to-date sales reached 2,269 units, over 11 per cent higher than last year and on pace to hit a new record high. The growth in sales was possible thanks to a boost in new listings this year. However, the gains in new listings did little to impact inventory levels which remained well below levels traditionally seen in the market in October.

While conditions are not as tight as they were earlier in the year, the months of supply remained exceptionally tight at one and a half months. Despite persistently tight conditions, prices have trended lower from the earlier highs. Airdrie hit a record high price back in April of this year at $510,700, prices have since fallen by six per cent since then yet remain over 14 per cent higher than levels reported last year.

Cochrane

A pullback in new listings relative to sales activity caused the sales-to-new-listings ratio to push up to 90 per cent once again, causing inventories to trend down relative to last month. While overall inventories still remain higher than the exceptionally low levels seen last year, levels are still well below what is typically seen in the market.

While prices have eased off recent highs, at a benchmark price of $507,000, prices remain over 16 per cent higher than last years levels. Price growth has been mostly driven by the detached and semi-detached sector which have reported year-over-year gains exceeding 18 per cent.

Okotoks

A pullback in new listings likely weighed on sales this month as the sales-to-new-listings ratio pushed above 100 per cent causing inventories to remain exceptionally low for October. While conditions are still not as tight as they were earlier in the year, the shift this month did little to support more balanced conditions.

Persistently tight conditions did slow the pace of adjustment in prices as the benchmark price was $537,800 in October. While prices have eased from the high reported in May, they remain over 11 per cent higher than last years levels.

版权声明:【除原创作品外,本公众号所使用的文章、图片、视频及音乐收集整理于网络,其版权属于相关权利人所有,只为方便卡城华人,如存在不当使用的情况,敬请相关权利人随时与我们联系及时处理。】

如果觉得文章有帮助,把它分享出去,帮助更多的人,

|

|

发表于 2022-12-16 16:42:47

发表于 2022-12-16 16:42:47